Study Demonstrates Positive Economics for a Second Plant Supplied with Spodumene Concentrate from Existing Partnerships

Piedmont Lithium Inc. (“Piedmont” or the “Company”) is pleased to report the results of a Preliminary Economic Assessment (“PEA” or “Study”) for a proposed merchant lithium hydroxide plant (“LHP-2”) to expand Piedmont’s planned U.S. manufacturing capacity to 60,000 t/y of lithium hydroxide. The LHP-2 PEA results demonstrate the potential for Piedmont Lithium to expand its lithium hydroxide manufacturing business using spodumene concentrate from market sources, including under existing offtake agreements with Sayona Quebec and Atlantic Lithium.

“2021 was a transformative year for electrification in the United States,” said Piedmont President and CEO Keith Phillips. “Current and forecasted battery manufacturing capacity now exceeds 500 gigawatt-hours (“GWh”) with public announcements of over $25 billion in capital investments to occur by 2025. The potential lithium volume these battery plants will require reinforces the importance of developing a domestic lithium supply chain and solidifies our decision to aggressively evaluate and pursue expansion opportunities for a second lithium hydroxide plant. The planned 2023 restart of North American Lithium in conjunction with our partner, Sayona Mining, and potential for spodumene production at Ewoyaa in partnership with Atlantic Lithium as early as 2024 ensures that our LHP-2 operations will have dedicated material supply from day one. With prevailing spot lithium prices at approximately triple the fixed pricing assumptions used in the PEA, Piedmont has substantial leverage relative to higher lithium prices across our entire portfolio of projects,” commented Phillips.

The planned LHP-2 project economics are shown alongside the Company’s flagship Carolina Lithium Project in the table below. Both projects are shown using fixed prices of $22,000 per tonne LiOH and $1,200 per tonne for spodumene concentrate. The economic model for LHP-2 was developed based on common physical and operating characteristics of multiple potential plant locations currently under evaluation for final site selection. LHP-2 development remains subject to, among other things, a final site selection and financing. Piedmont plans to advance Carolina Lithium, LHP-2, Ewoyaa, and NAL restart on the earliest practical timelines, subject to permitting and regulatory approvals for each project.

|

Unit |

LHP-2 | Carolina Lithium[1] | |

|---|---|---|---|

|

Operation life |

years |

30 |

30 |

|

Steady state annual lithium hydroxide production |

t/y |

30,000 |

30,000 |

|

Total initial capital cost |

$mm |

$572 |

$988 |

|

After tax Net Present Value @ 8% discount rate |

$mm |

$2,248 |

$2,843 |

|

After tax Internal Rate of Return |

% |

33% |

34% |

|

Steady-state LiOH production all in sustaining costs |

$/t |

$10,630 |

$4,377 |

|

Average annual steady state EBITDA |

$mm/y |

$346 |

$592 |

|

Average annual steady state after-tax cash flow |

$mm/y |

$269 |

$385 |

“We are very pleased with the results of the Preliminary Economic Assessment for our second planned U.S. lithium hydroxide plant. The Project’s economics are outstanding using a fixed price deck that is at a 66% discount to prevailing spot prices. With many analysts projecting lithium shortages to grow into the 2030s, the Project offers substantial leverage relative to possible higher lithium prices.

We aspire to be America’s leading producer of lithium hydroxide, and at 60,000 tonnes per year Piedmont’s planned capacity would be approximately quadruple the entire domestic installed base today, positioning us to be a critical supplier to the U.S. supply chain. With long-term supply agreements in place with our partners Atlantic Lithium and Sayona Mining, we have locked in the raw material we require for this expansion, enabling us to control our own destiny while capturing the economics of the integrated production process.

Our focus for the remainder of 2022 turns to ‘execution,’ with four major projects under development. Along with our partners, we are targeting first spodumene concentrate production at North American Lithium in 2023, and at the Ewoyaa Project in Ghana in 2024. U.S. lithium hydroxide production will follow, with our integrated Carolina Lithium Project and LHP-2 to be advanced on the earliest practical timelines. Lithium markets are strong, and we are fortunate to possess a strong project pipeline to capitalize on the generational opportunity presented by the electrification of the vehicle business.

Keith D. Phillips, President and Chief Executive Officer

LIOH CONVERSION PLANT – PRELIMINARY ECONOMIC ASSESSMENT

This PEA of Piedmont Lithium’s proposed LHP-2 is based on a 30,000 t/y lithium hydroxide conversion facility that features Metso:Outotec conversion technology and includes spodumene concentrate receiving/short term storage facilities, reagent receiving and storage facilities, process facilities, and site infrastructure. The LHP-2 project contemplates a 30-year operation. The ramp-up period for LHP-2 operations is assumed to achieve nameplate capacity, including both overall production and battery quality production, after a 12-month ramp-up period. Table 2 provides a summary of production and cost figures for the LHP-2 project. All values are reported in U.S. dollars. The PEA economics for LHP-2 as presented exclude the potential returns related to profits from spodumene concentrate sales from Sayona or Atlantic Lithium attributable to Piedmont for our project-level and parent company investments in those companies.

|

Unit |

Estimated Value | |

|---|---|---|

|

Annual Production | ||

|

Operation life |

years |

30 |

|

Steady state annual lithium hydroxide production |

t/y |

30,000 |

|

Average annual spodumene concentrate (SC6) purchases |

t/y |

196,000 |

|

Operating and Capital Costs | ||

|

Steady-state LiOH production all in sustaining costs (“AISC”) |

$/t |

$10,630 |

|

Development capital |

$mm |

$480 |

|

Other owner’s costs |

$mm |

$28 |

|

Contingency |

$mm |

$64 |

|

Total initial capital cost |

$mm |

$572 |

|

Sustaining and deferred capital |

$mm |

$163 |

|

Working capital |

$mm |

$128 |

|

Financial Performance | ||

|

After tax Net Present Value (“NPV”) @ 8% discount rate |

$mm |

$2,248 |

|

After tax Internal Rate of Return (“IRR”) |

% |

33% |

|

Average annual steady state EBITDA |

$mm/y |

$346 |

|

Average annual steady state after-tax cash flow |

$mm/y |

$269 |

|

Payback from start of operations |

years |

3.1 |

Study Consultants

This PEA combines information and assumptions provided by a range of independent consultants, including the following consultants who have contributed to key components of the Study.

|

Table 3: PEA Study Consultants | |

|

Consultant |

Scope of Work |

|

Primero Group Americas Inc. |

Lithium hydroxide plant design and overall Study integration |

|

Metso:Outotec |

Lithium hydroxide manufacturing technology package |

|

Benchmark Mineral Intelligence |

Lithium products marketability |

30,000 t/y Lithium Hydroxide Plant Overview

The Study assumes that Piedmont Lithium’s LHP-2 will be located on one of several sites under consideration that share similar characteristics with respect to acreage, infrastructure, rail access, proximity to transportation routes, potential customers, and available workforce. While a final site has not been selected, co-locating LHP-2 at the existing Carolina Lithium Project site in Gaston County, NC is not being considered.

This PEA assumes that LHP-2 will operate for 30 years and produce 30,000 t/y of lithium hydroxide at steady state from approximately 196,000 t/y of SC6 delivered from third party spodumene concentrate purchases. To support LHP-2 operations, our strategy is to work with Atlantic Lithium to develop the Ewoyaa Project in Ghana, where Piedmont Lithium holds offtake rights to 50% of spodumene concentrate production on a life-of-mine basis. The Ewoyaa Project is subject of a Scoping Study published by Atlantic Lithium with a Production Target of 300,000 t/y of SC6.

In addition, SC6 may be purchased from Sayona Quebec, where Piedmont Lithium holds offtake rights for the greater of 113,000 t/y, or 50% of SC6 production on a life-of-mine basis, from the North American Lithium and Authier Projects. As of March 2022, North American Lithium is the subject of active restart efforts with a forecasted restart in 2023.

The financial results reported in this announcement do not capture the potential income or associated investment requirements from Piedmont’s equity interests in Sayona Quebec or Atlantic Lithium.

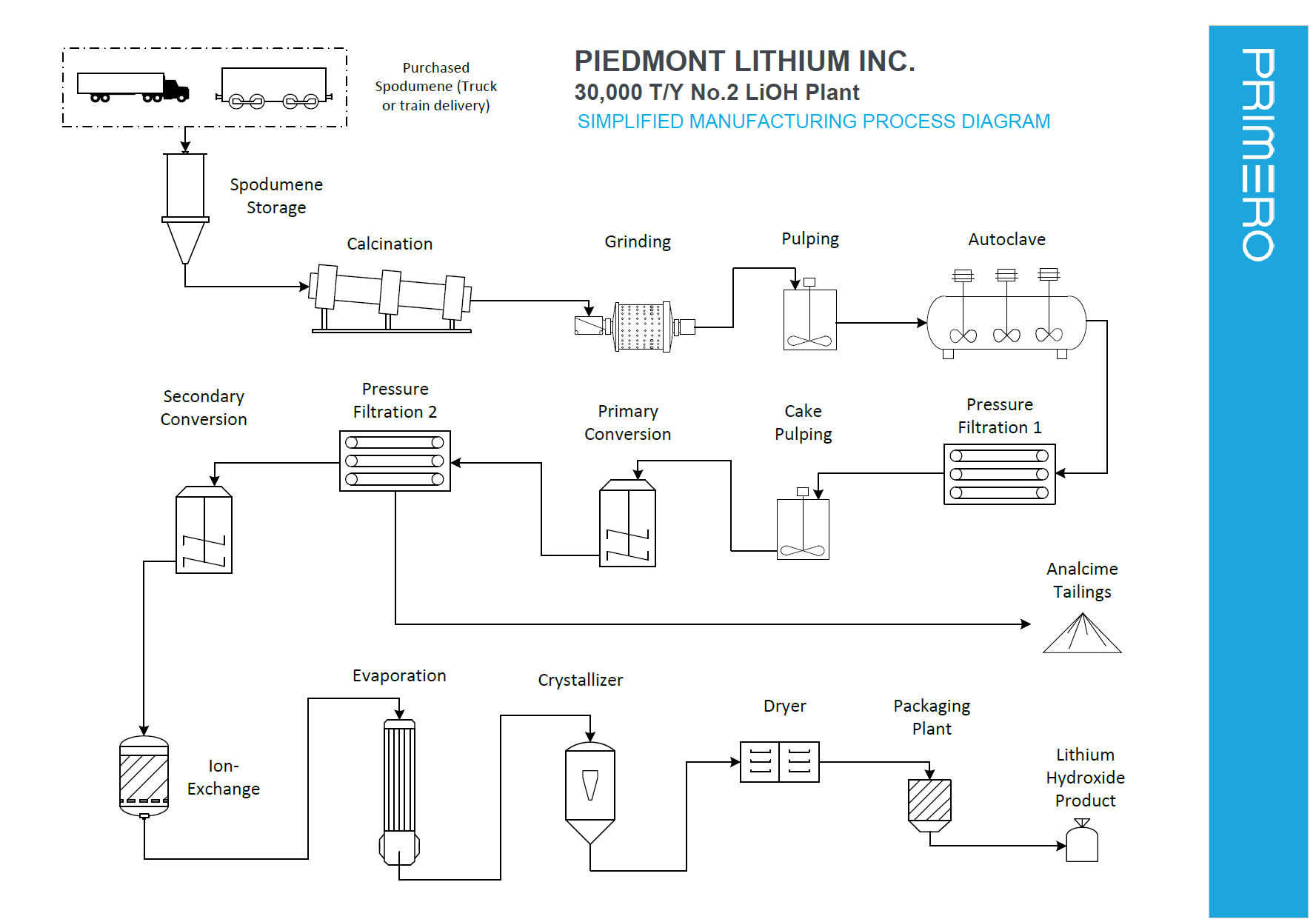

Process Design

In 2021, Piedmont engaged Metso:Outotec to undertake pilot plant testwork using their proprietary alkaline pressure leach process for production of lithium hydroxide monohydrate. The spodumene concentrate sample used was produced during concentrator pilot plant operation in 2020 from samples collected from the Carolina Lithium Project. The spodumene concentrate was calcined by Metso:Outotec at their laboratory in Oberursel, Germany. The calcined concentrate was then sent to Metso:Outotec Research Center in Pori, Finland for hydrometallurgical testing.

This PEA assumes that the recovery and quality of lithium hydroxide monohydrate produced from third party spodumene concentrates, including Atlantic Lithium or North American Lithium, would be identical to the estimated grade and quality of lithium hydroxide monohydrate referenced in the Company’s Carolina Lithium Project Feasibility Study. Additional testwork in connection with this PEA was not undertaken.

The pilot plant flowsheet tested included: soda leaching, cold conversion, secondary conversion, ion exchange, and lithium hydroxide crystallization. The pilot plant operated for approximately 10 days. Roughly 100 kg of calcined spodumene concentrate was fed to the pilot plant. The average total lithium extraction achieved in soda leaching and cold conversion was 89% during the first 136 hours of operation. Process recycles were incorporated in the pilot plant with no significant accumulation of impurities in the process. First stage lithium hydroxide crystallization was operated continuously during the pilot plant. Second stage crystallization was operated in batches after the completion of the continuous pilot plant. Impurities levels in the final battery-quality lithium hydroxide monohydrate product were typically low with Al <10 ppm, Ca <10 ppm, Fe <20 ppm, K <10 ppm, and Si <40 ppm. All other metal impurities were below detection limits.

Based on the testwork completed, Metso:Outotec expects that 196,000 t/y of SC6 will be required to produce 30,000 t/y of battery quality lithium hydroxide. Based on Metso:Outotec’s estimate, this PEA study assumes a 91% lithium conversion rate through the lithium hydroxide conversion plant.

Site Plan

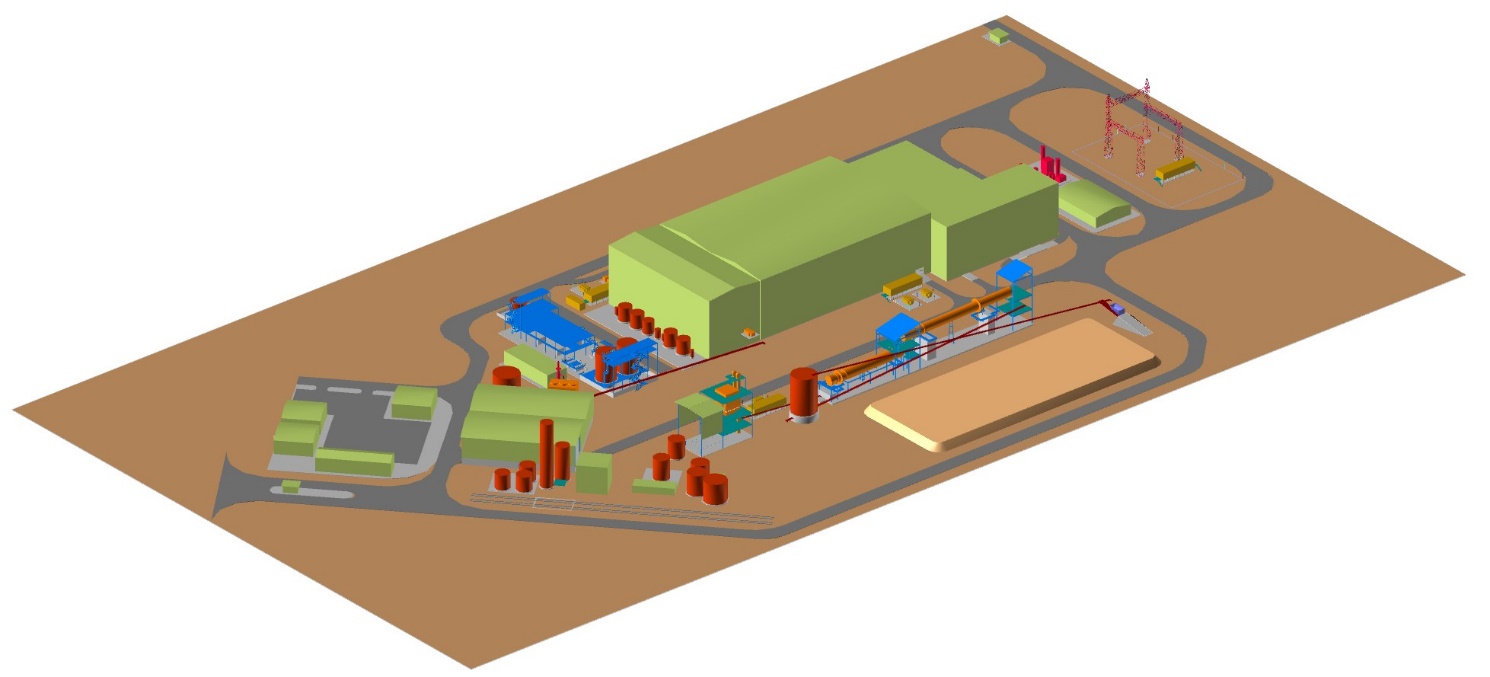

A preliminary integrated site plan and 3D model of a potential plant including lithium hydroxide manufacturing, rail siding and ancillary facilities was developed by Primero Group during the course of the study. Figure 2 shows an indicative site plan for the manufacturing facility on a generic site. The financial and operating model supports the capital cost estimate and could be used as the basis for subsequent stages of engineering related to a final LHP-2 location.

Infrastructure Each site being considered offers an attractive infrastructure location as related to major interstate access, rail, and ports, along with support services such as fabrication, maintenance, and technical service contractors. Temporary or permanent camp facilities will not be required as part of the LHP-2 project.

Logistics

Each considered location allows for spodumene concentrate to be delivered to LHP-2 for processing by rail, rail siding, or by truck from a port within 300 miles of the site. For spodumene concentrate pricing, the PEA assumes that Piedmont can buy SC6 at a market price on a CIF Port of Charleston, SC, basis plus an allowance of $35/t for inland transportation.

Permitting

Each site being considered is located on private land. The permitting timeline of the LHP-2 Project is assumed to be similar for each of the sites under consideration. The current development schedule assumes that a non-Title V air permit will be required for the project and that hydroxide conversion solid residue can be disposed of at an existing permitted facility that can receive non-hazardous solid waste.

Marketing

Lithium Market Outlook

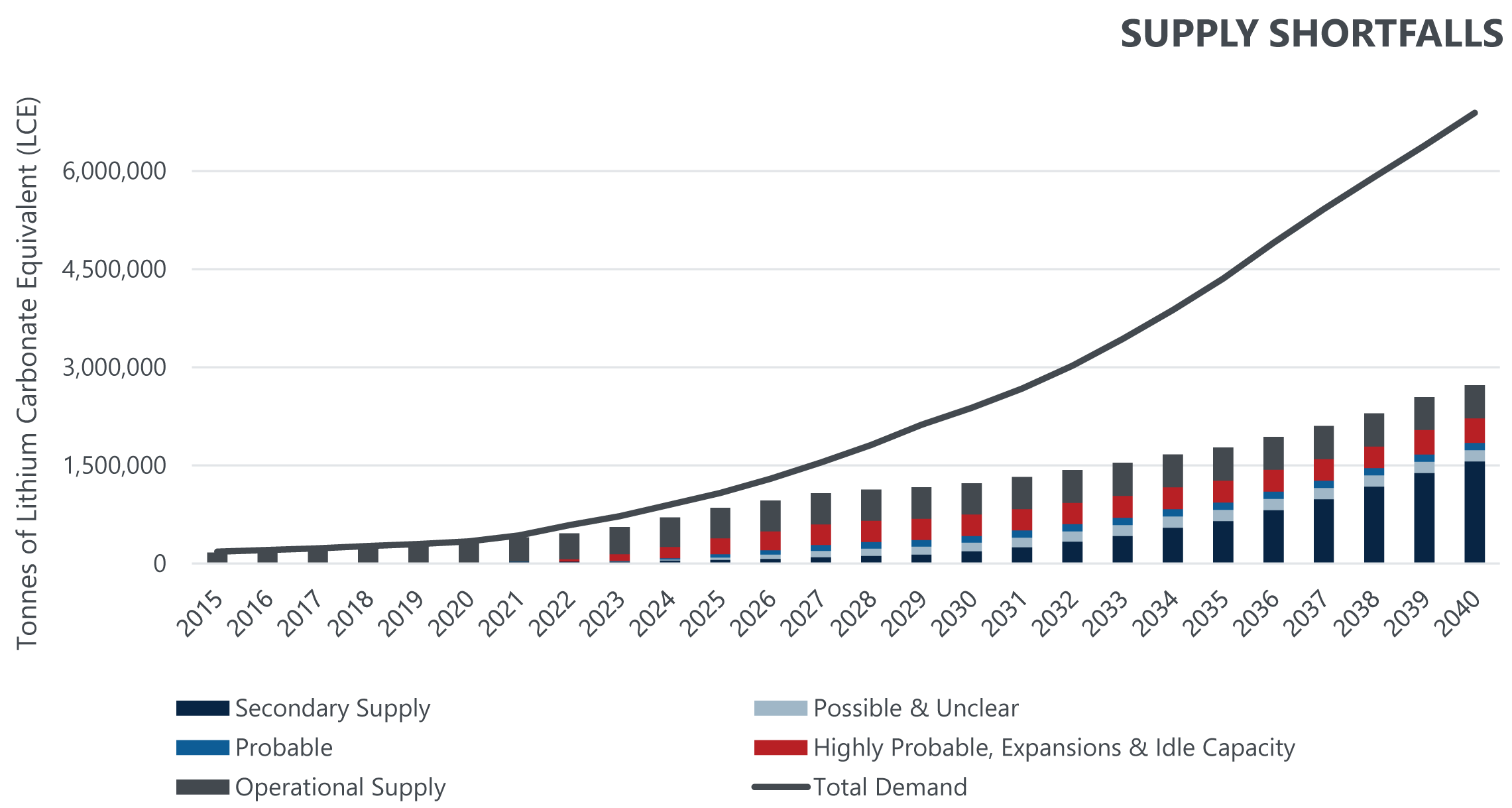

Benchmark Mineral Intelligence (“Benchmark”) reports that total battery demand grew to nearly 400 GWh in 2021 translating to 357kt of lithium carbonate equivalent (“LCE”) demand in 2021, a growth of 59% over 2020 demand. Benchmark calculated total demand in 2021 to be 492kt on an LCE basis. Benchmark further expects the market to remain in a structural deficit (see Figure 3) for the foreseeable future as demand outpaces supply.

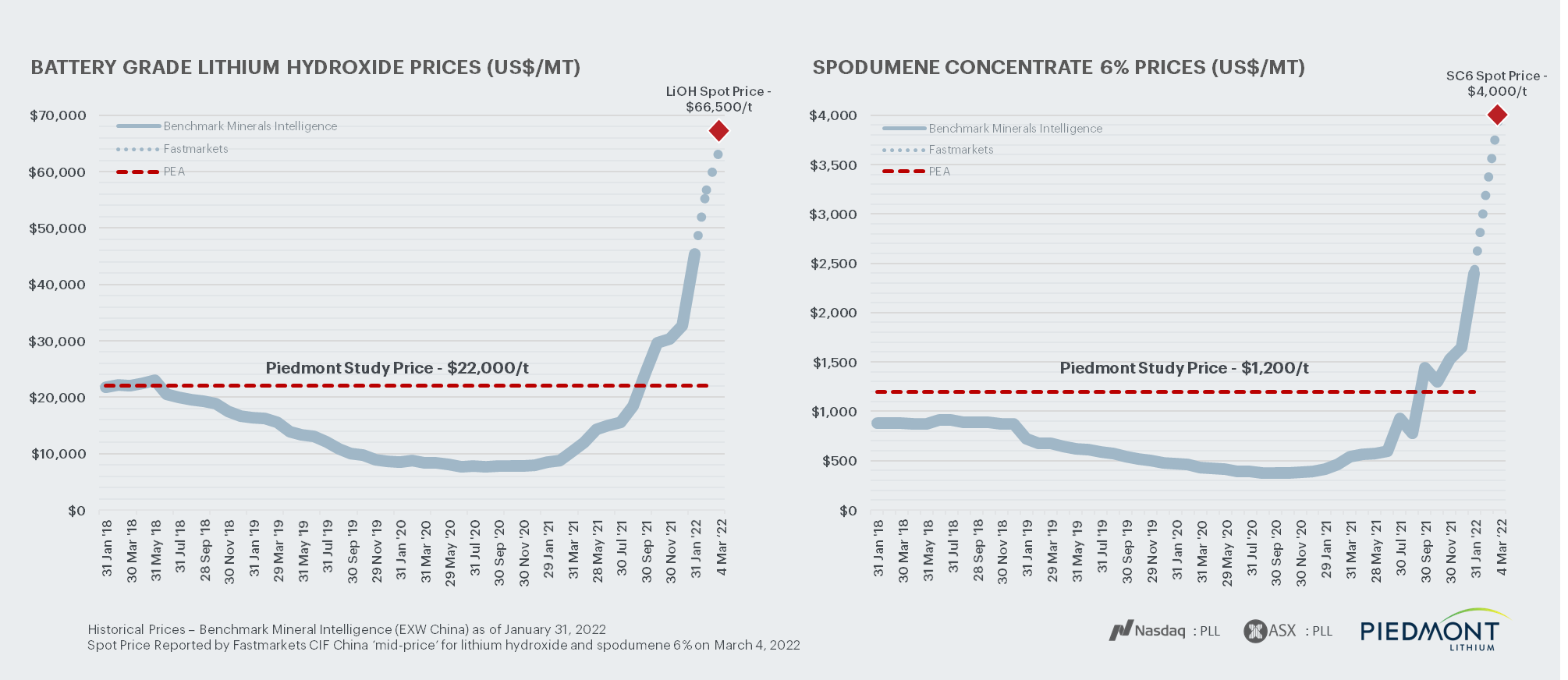

Lithium prices have risen dramatically since Piedmont published the feasibility study for Carolina Lithium in December 2021, with current spot prices for battery-grade lithium hydroxide now exceeding $65,000/t and contract prices doubling from 2021 levels. Several market analysts have raised their pricing projections for lithium hydroxide (Table 4) over the medium-term.

Fixed prices of $22,000/t for lithium hydroxide and $1,200/t for spodumene concentrate for the life of the project have been assumed in this PEA. Figure 4 compares the pricing used in the study to historical pricing for lithium hydroxide and spodumene concentrate.

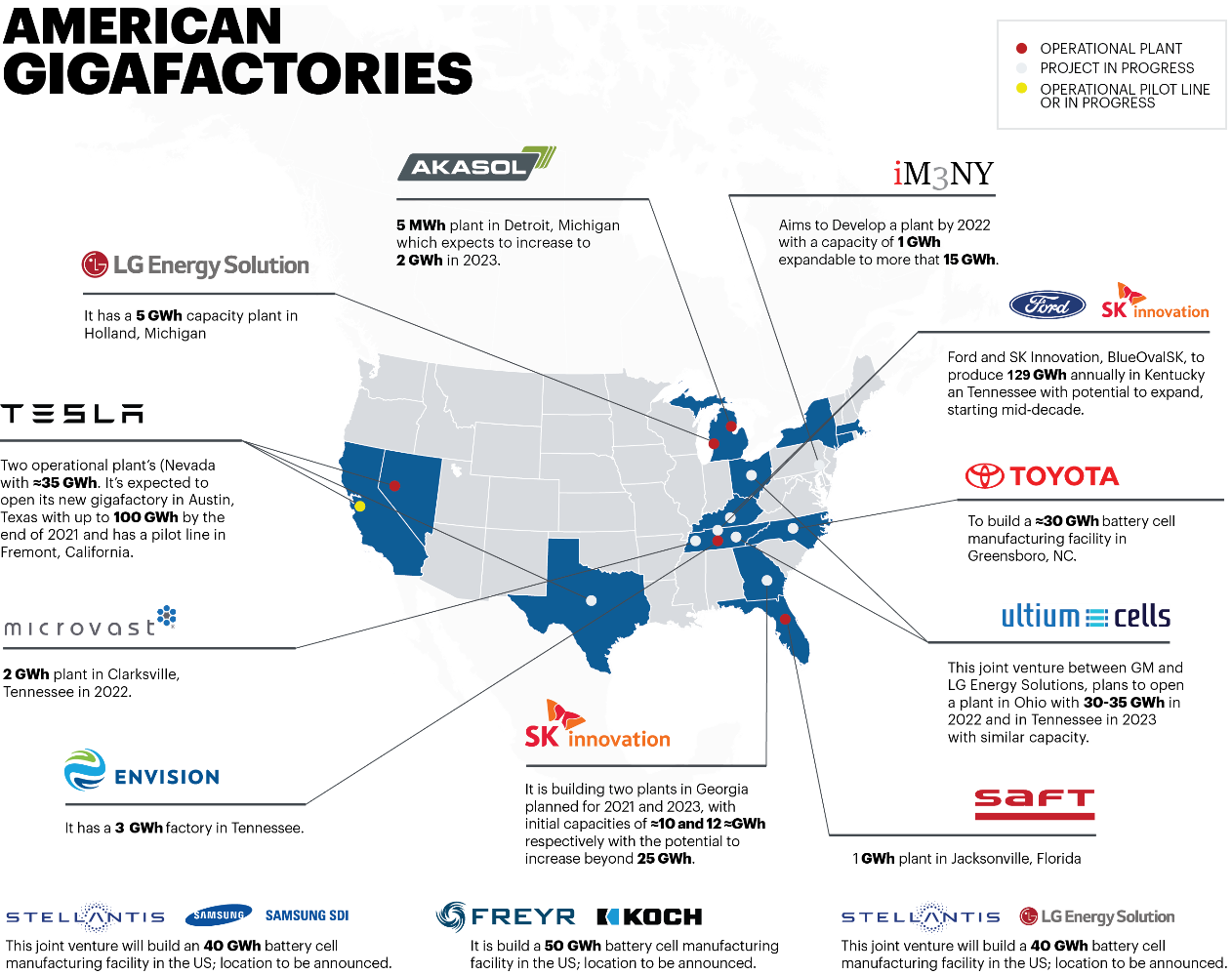

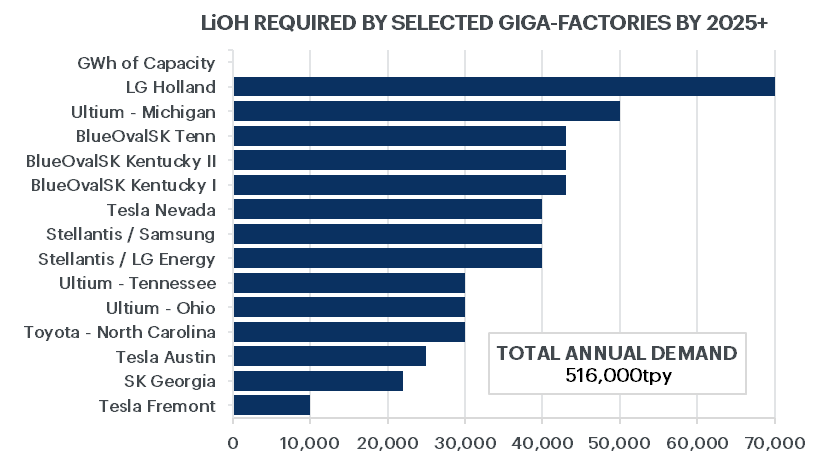

As shown in Figure 5 below North America is seeing considerable growth in battery plant capacity. Figure 6 below shows the corresponding lithium hydroxide demand for the announced U.S. battery plant capacity at full production.

Market Strategy

Piedmont is focused on establishing strategic partnerships with customers for battery grade lithium hydroxide with an emphasis on a customer base which is focused on EV demand growth in North America and Europe. Piedmont will concentrate this effort on these growing EV supply chains, particularly in light of the growing commitments of battery manufacturing by groups such as Ford, General Motors, Stellantis, Toyota, LGES, SK Innovation, Samsung SDI, and others. Advanced discussions with prospective customers are ongoing.

Operating and Capital Costs

The lithium hydroxide conversion plant contemplated in this PEA is substantially identical to the lithium hydroxide conversion plant modeled as part of the fully-integrated Carolina Lithium bankable feasibility study published by Piedmont in December 2021. The operating and capital costs, including sustaining capital costs, reflected in that BFS for conversion costs only, excluding mining and concentration, have largely been utilized in this PEA and are the result of detailed scrutiny at the bankable feasibility study level. Site-specific operating and capital costs for LHP-2 have been estimated at a PEA level; these site-specific costs will be updated in future technical studies after a final site selection.

Operating Cost Estimates

The operating cost estimate was prepared based on producing 30,000 t/y of lithium hydroxide monohydrate at the LHP-2 project. Table 5 summarizes the estimated average operating costs during steady state operations.

The operating cost estimate is based on Q4 2021 U.S. dollars with no escalation. Target accuracy of the operating cost estimate is ± 30%. Operating costs are based on steady-state production. The average operating costs include the commissioning and ramp-up of chemical plant operations.

Capital Cost Estimates

Table 6 highlights the total estimated capital expenditures for the LHP-2 project. Variable contingency has been applied to project costs based on the level of engineering definition completed and the confidence level of supplier and contractor quotations. The capital cost estimate has a ±30% accuracy and is based on Q4 2021 costs.

|

Cost Center |

Total Capital Costs ($mm) |

|---|---|

|

Direct development costs |

$423.3 |

|

Project indirects |

$56.9 |

|

Owner’s costs |

$28.0 |

|

Contingency |

$63.9 |

|

Total Development Capital |

$572.1 |

|

Deferred and sustaining capital |

$163.3 |

|

Working capital |

$127.9 |

Project Schedule

An indicative project schedule was prepared as part of the PEA. The summary schedule is presented in Figure 7. For the purposes of financial modeling, a project investment decision and ordering of long lead items for LHP-2 is assumed to commence at the start of Project Year 1. This schedule is indicative only and project approvals including receipt of all permits will be required before construction activities can commence on the LHP-2 project.

Commercial production at the lithium hydroxide plant is estimated to start 24 months after the start of construction, with full production achieved within 12 months from the start of production.

Royalties, Taxes, Depreciation, and Depletion

The LHP-2 project economics include the following key parameters related to royalties, tax, and depreciation allowances.

- The LHP-2 project relies on third party spodumene concentrate purchases, so no royalties are applied to the model.

- Model assumes North Carolina state corporate taxes are 2.5% but will reduce to 0% between 2024-2028

- Federal tax rate of 21% is applied and state corporate taxes are deductible from this rate

- Effective base tax rate of 22.975% in 2028 and reduces to 21% from 2028 onwards

- Depreciation in the lithium hydroxide plant is based on Asset Class 28.0 – Mfg. of Chemical and Allied Products in Table B-1 using GDS of 5 years with the double declining balance method

- Bonus depreciation of 80% has been applied based on the bonus depreciation allowance in the Tax Cuts and Jobs Act of 2017, where applicable

Modeling Assumptions

A detailed project economical model was completed by Primero as part of the study with the following key assumptions:

- Capital and operating costs are in accordance with technical study outcomes

- Chemical plant ramp-up is based on a 12-month time frame to nameplate production

- Financial modeling has been completed on a yearly basis, including estimated cash flow for construction activities and project ramp-up

- Pricing information for battery-grade lithium hydroxide sales and spodumene concentrate supply are based on a fixed price of $22,000/t for battery quality lithium hydroxide and $1,200/t for 6.0% Li2O spodumene concentrate

- Royalties, tax, and depreciation allowances according to stated assumptions

Financial Modelling

This PEA assumes a chemical plant production life of 30 years. The chemical plant operates using market procurement of SC6, including potentially from offtake sources currently controlled by or contracted with Piedmont.

The current economic model is based on a yearly projection of capital costs and assumes that the full capital cost is spent across 2 years prior to the commissioning of the chemical plant. The chemical plant is assumed to ramp to full production over a one-year period.

Payback Period

Payback periods for the LHP-2 project constructed in a single phase is 3.1 years after the start of chemical plant operations or 4.6 years from the start of construction. Payback period is calculated on the basis of after-tax free cash flow.

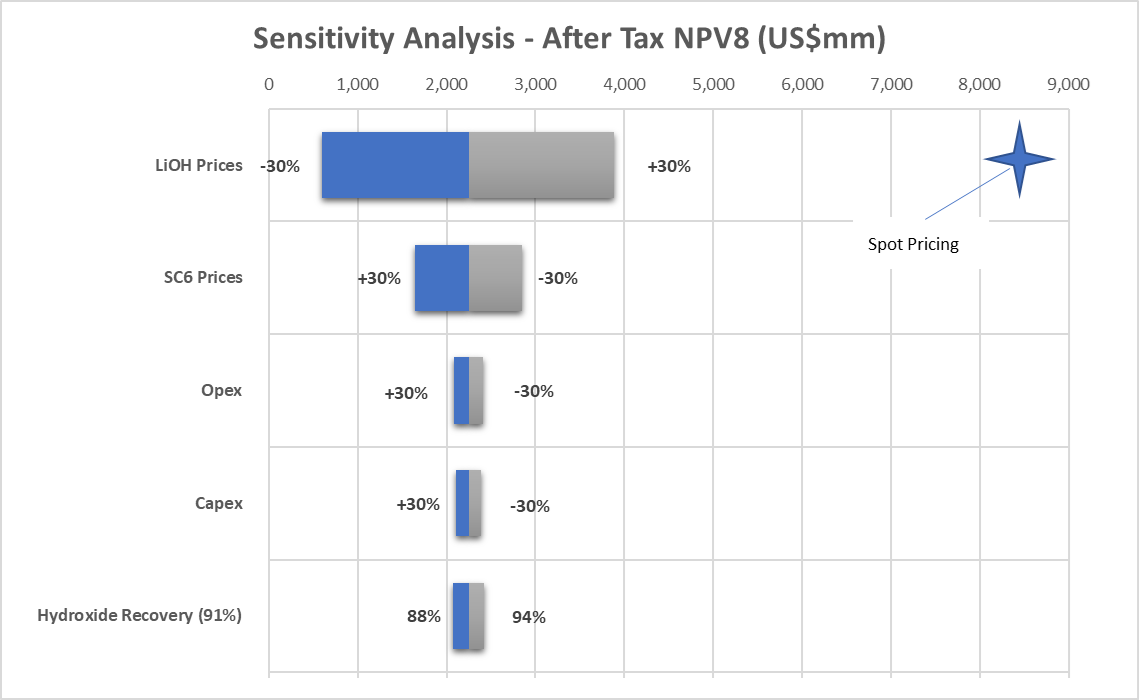

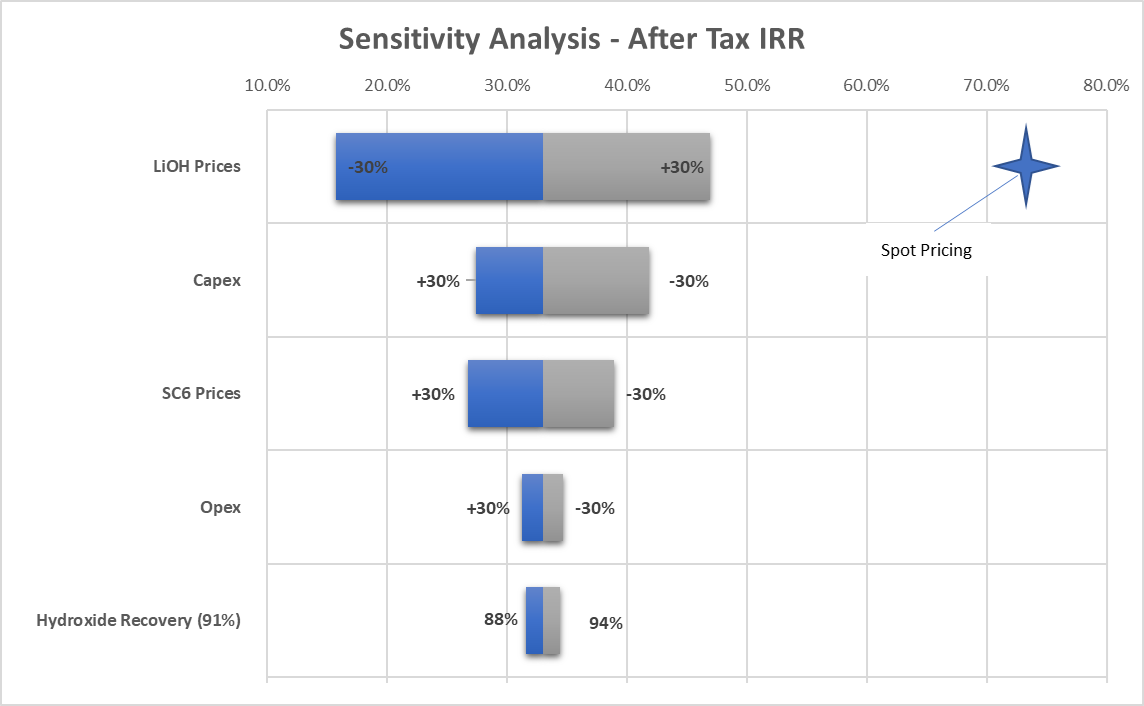

Sensitivity Analyses

Key inputs into this preliminary economic assessment have been tested by pricing, capital cost, and operating cost sensitivities. The impact to after tax net present value is presented in Figure 8 while impact to project IRR is presented in Figure 9. Additionally, applying discount rates of 7% and 9% resulted in NPV7 of $2,560mm and NPV9 of $1,981mm.

A further sensitivity analysis showed that, when holding constant the assumption that long-term forecasted SC6 prices will be 5.5% of lithium hydroxide prices, each $1,000 increase in lithium hydroxide prices leads to an increase in Project NPV of approximately $156mm and steady-state EBITDA of $20mm per year. Applying current spot prices to the PEA financial model[2] results in an after-tax net present value of $8.6bb and a steady-state EBITDA of $1.1bb per year. Using spot prices at Carolina Lithium would result in an after-tax net present value of $11.8bb and steady-state EBITDA during integrated operations of $2.0bb.

Conclusions and Next Steps

The LHP-2 PEA Study results demonstrate the potential for Piedmont Lithium to expand its lithium hydroxide manufacturing business using imported spodumene concentrate from market sources, including existing offtake agreements which the Company secured in 2021. The Company will now concentrate on the following initiatives to drive the LHP-2 project forward:

- Finalize site selection for LHP-2 operations.

- Undertake further technical studies associated with LHP-2.

- Selection of a Front-End Engineering Design (“FEED”) and EPC contractor for execution of the LHP-2 project.

- Submit a second loan application to the Department of Energy’s Loan Program Office under the Advanced Technology Vehicle Manufacturing program for LHP-2.

- Incorporate LHP-2 into ongoing strategic discussions led by financial advisors Evercore and J.P. Morgan.

Forward Looking Statements

This announcement includes forward-looking statements within the meaning of applicable securities laws, including statements about LHP-2, the potential selection of a site for such plant, timing and expectations around any development and production of the plant and estimates and assumptions around permitting, revenues and costs of the plant. These forward-looking statements are based on Piedmont’s expectations and beliefs concerning future events. Such forward-looking statements concern Piedmont’s anticipated results and progress of its operations in future periods, planned exploration and, if warranted, development of its properties and plans related to its business and other matters that may occur in the future. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. All statements contained herein that are not clearly historical in nature are forward-looking, and the words “anticipate,” “believe,” “expect,” “estimate,” “may,” “might,” “will,” “could,” “can,” “shall,” “should,” “would,” “leading,” “objective,” “intend,” “contemplate,” “design,” “predict,” “potential,” “plan,” “target” and similar expressions are generally intended to identify forward-looking statements.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking statements. Such factors include, among others, risks related to:

- the risk that anticipated plans, development, production, revenues or costs are not attained;

- Piedmont’s operations being further disrupted and Piedmont’s financial results being adversely affected by public health threats, including the novel coronavirus pandemic;

- Piedmont’s limited operating history in the lithium industry;

- Piedmont’s status as a development stage company, including Piedmont’s ability to identify lithium mineralization and achieve commercial lithium mining;

- mining, exploration and mine construction, if warranted, on Piedmont’s properties, including timing and uncertainties related to acquiring and maintaining mining, exploration, environmental and other licenses, permits, access rights or approvals in Gaston County, North Carolina, the Province of Quebec, Canada and Cape Coast, Ghana as well as properties that Piedmont may acquire or obtain an equity interest in the future;

- completing required permitting activities required to commence processing operations for the LHP-2 Project;

- Piedmont’s ability to achieve and maintain profitability and to develop positive cash flows from Piedmont’s processing activities;

- Piedmont’s estimates of mineral reserves and resources and whether mineral resources will ever be developed into mineral reserves;

- investment risk and operational costs associated with Piedmont’s exploration activities;

- Piedmont’s ability to develop and achieve production on Piedmont’s properties;

- Piedmont’s ability to enter into and deliver products under supply agreements;

- the pace of adoption and cost of developing electric transportation and storage technologies dependent upon lithium batteries;

- Piedmont’s ability to access capital and the financial markets;

- recruiting, training and developing employees;

- possible defects in title of Piedmont’s properties;

- compliance with government regulations;

- environmental liabilities and reclamation costs;

- estimates of and volatility in lithium prices or demand for lithium;

- Piedmont’s common stock price and trading volume volatility;

- the development of an active trading market for Piedmont’s common stock;

- Piedmont’s failure to successfully execute our growth strategy, including any delays in Piedmont’s planned future growth; and

- other factors set forth in Piedmont’s most recent Annual Report on Form 10-K and subsequent reports, as filed with the U.S. Securities and Exchange Commission.

All forward-looking statements reflect Piedmont’s beliefs and assumptions based on information available at the time the assumption was made. These forward-looking statements are not based on historical facts but rather on management’s expectations regarding future activities, results of operations, performance, future capital and other expenditures, including the amount, nature and sources of funding thereof, competitive advantages, business prospects and opportunities. By its nature, forward-looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, known and unknown, that contribute to the possibility that the predictions, forecasts, projections or other forward-looking statements will not occur. Although Piedmont have attempted to identify important factors that could cause actual results to differ materially from those described in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, believed, estimated, or expected. Piedmont cautions readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. Except as otherwise required by the securities laws of the United States, Piedmont disclaims any obligation to subsequently revise any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events. Piedmont qualifies all the forward-looking statements contained in this release by the foregoing cautionary statements

Illustrative financial outcomes for the Carolina Lithium Project when applying a fixed price of $22,000 per metric tonne of lithium hydroxide and $1,200 per metric tonne of spodumene concentrate to the Carolina Lithium financial model. Results are Company estimates and indicative only and are not independently verified by the Carolina Lithium BFS Qualified Persons. ↑

Applying an assumption of $66,500/t for lithium hydroxide and $4,000/t for spodumene concentrate as the fixed pricing assumption within the Carolina Lithium and LHP-2 financial models based on current spot pricing as reported by Fastmarkets on March 7, 2022. ↑

For further information, contact:

Malissa Gordon

VP, Government Affairs

T: +1 704 491 9130

E: mgordon@piedmontlithium.com

Investor Relations

John Koslow

FP&A and Investor Relations Manager

T: +1 516 320 0842

E: jkoslow@piedmontlithium.com